To maintain profitability, there are two essential metrics for home improvement contractors to know: credit card availability and home equity availability. Knowing these isn’t just a “nice to have”—it is the difference between a high-margin year and a business-killing overhead.

Most contractors still run their businesses exactly the way their grandfathers did: book the lead, knock the door, deliver a high-energy pitch, and then “pray for approval.” In a tightening credit environment, this is a recipe for Sales Team Burnout.

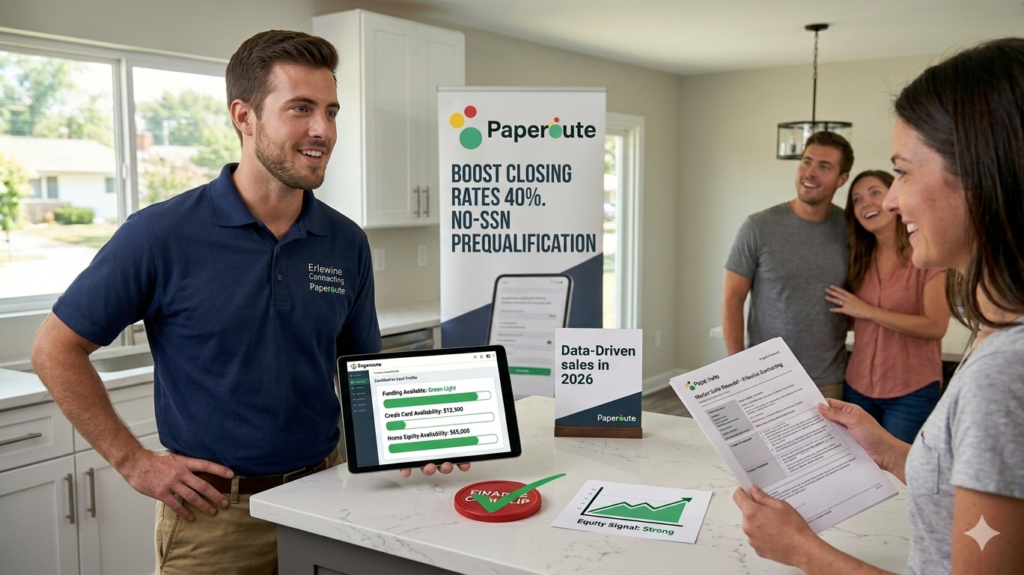

When you wait until the end of a three-hour presentation to talk money, you aren’t just risking a “no”—you are risking your company’s sales momentum. The advantage in 2026 shifts to the contractor who knows a lead’s ability to fund the project before the rep ever enters the home. Using soft credit pulls to identify funding lanes is how you protect margins while your competitors waste time on “Dead on Arrival” leads.

Contractors make money on two things: efficiency and close rate. When you can see a homeowner’s mortgage balance and equity signal upfront, you stop selling blind.

Knowing home equity availability allows your team to:

<a name=”credit”></a>

While equity covers the big ticket, credit card availability is the “bridge” that saves deals. Most contractors guess at a customer’s liquid capacity; the top 5% of earners in our industry know.

Seeing credit card balances and available limits tells your rep:

There is a massive psychological advantage to lead prequalification. When a homeowner discovers they can qualify before the rep shows up, the nature of the appointment changes.

The conversation shifts from: “Can we even afford to do this?” to: “What style of cabinets do we want?” By using a lead intelligence platform, you turn the appointment into an actual buying conversation. This one shift changes the tone of the call, the body language in the kitchen, and the likelihood of a positive outcome. Your reps stop being “closers” who hope for the best and start being “consultants” who execute a data-backed plan.

This is exactly why Paperoute exists. We allow contractors to run a soft pull with no impact to the customer’s credit score. In a single, simple snapshot, you see the true capacity of the buyer:

Paperoute turns your team from order-takers into strategists. You instantly know if the buyer is in the Cash/Equity Lane, the Revolving Card Lane, or the Financing Lane.

The bottom line is simple: contractors should not enter a home without knowing how the homeowner plans to fund the project. That guessing costs time, destroys margins, and kills rep morale.

In 2026 and beyond, the winners in our industry will not be the contractors with the most leads—they’ll be the contractors who know their leads’ ability to buy before the appointment begins. That is the Paperoute advantage.e